Imagine you just handed over the keys to your new Westside property, only to have the central air give out during a record-breaking July heatwave. It is the ultimate post-closing headache, and it’s exactly why so many buyers and sellers ask: is a home warranty worth it in california? You might feel skeptical about whether these companies actually pay out or if they just hide behind fine print to deny your claims. I get it. In my years helping clients navigate the Los Angeles market, I’ve seen both the relief of a covered repair and the frustration of a “no.”

This guide will give you a clear framework to decide if a protection plan makes sense for your specific home. We’ll dive into the 2026 costs for California plans, which currently average between $42 and $83 per month, and explain how the California Department of Insurance protects you from unfair denials. You’ll also learn how to use a warranty as a strategic negotiation tool during escrow to protect your post-purchase cash flow. Whether you’re buying a mid-century gem or a new build, you’ll leave with a clear “yes or no” for your investment.

Key Takeaways

- Learn the legal distinction between standard home insurance and California “home protection contracts” to ensure your major systems are properly covered.

- Compare Westside LA repair prices against annual premiums to finally answer is a home warranty worth it in california for your specific budget.

- Discover how to use a home warranty strategically during the escrow process to smooth over negotiations and minimize post-closing friction.

- Identify common “fine print” traps regarding pre-existing conditions and see why your home inspection report is your best defense against claim denials.

- Use our summary decision matrix to determine if you should invest in a professional plan or “self-insure” using a dedicated high-yield savings account.

What is a Home Warranty in California? (Home Protection Contracts)

A home warranty is a service contract designed to cover the repair or replacement costs of your home’s major systems and appliances. While often confused with insurance, it operates on a different logic. If your refrigerator stops cooling or the heater fails due to normal wear and tear, the warranty kicks in. For many homeowners, the question of is a home warranty worth it in california boils down to how they prefer to manage risk. Instead of paying a large repair bill out of pocket, you pay a monthly premium and a smaller service call fee when a technician arrives at your door.

In the Golden State, these agreements are legally classified as “home protection contracts.” This distinction is vital because it places them under the direct oversight of the California Department of Insurance (CDI). Unlike some other states where the industry might feel less regulated, California requires these companies to be licensed and bonded. This provides you with a significant layer of consumer protection and a formal channel to file a complaint if a company fails to honor its contractual obligations. For a deeper dive into the history and general scope of these plans, you can check out this overview of What is a Home Warranty?

Home Warranty vs. Homeowners Insurance

Homeowners insurance is something your lender will require before you close on a Westside property. It covers sudden and accidental damage like fire, theft, or a tree falling on your roof. A home warranty is optional and covers the inevitable failure of mechanical parts. Think of insurance as your safety net for catastrophes. A warranty is your budget protection for maintenance. Lenders focus on the structure; warranties focus on the lifestyle inside that structure.

Quick comparison of coverage types:

- Home Insurance: Roof leaks, fire damage, theft, and personal liability.

- Home Warranty: HVAC systems, plumbing, electrical, and kitchen appliances.

The Legal Landscape: California Home Protection Acts

California law is quite specific about how these contracts are sold and managed. Under the California Civil Code, a home protection contract is defined as an agreement where a person or company promises to repair or replace home components for a predetermined fee. One of the best protections for local residents is the mandatory 30-day “free look” period. This allows you to cancel the contract within 30 days of purchase for a full refund, provided no claims have been made. This transparency ensures that deciding is a home warranty worth it in california doesn’t feel like a high-pressure trap with no exit strategy.

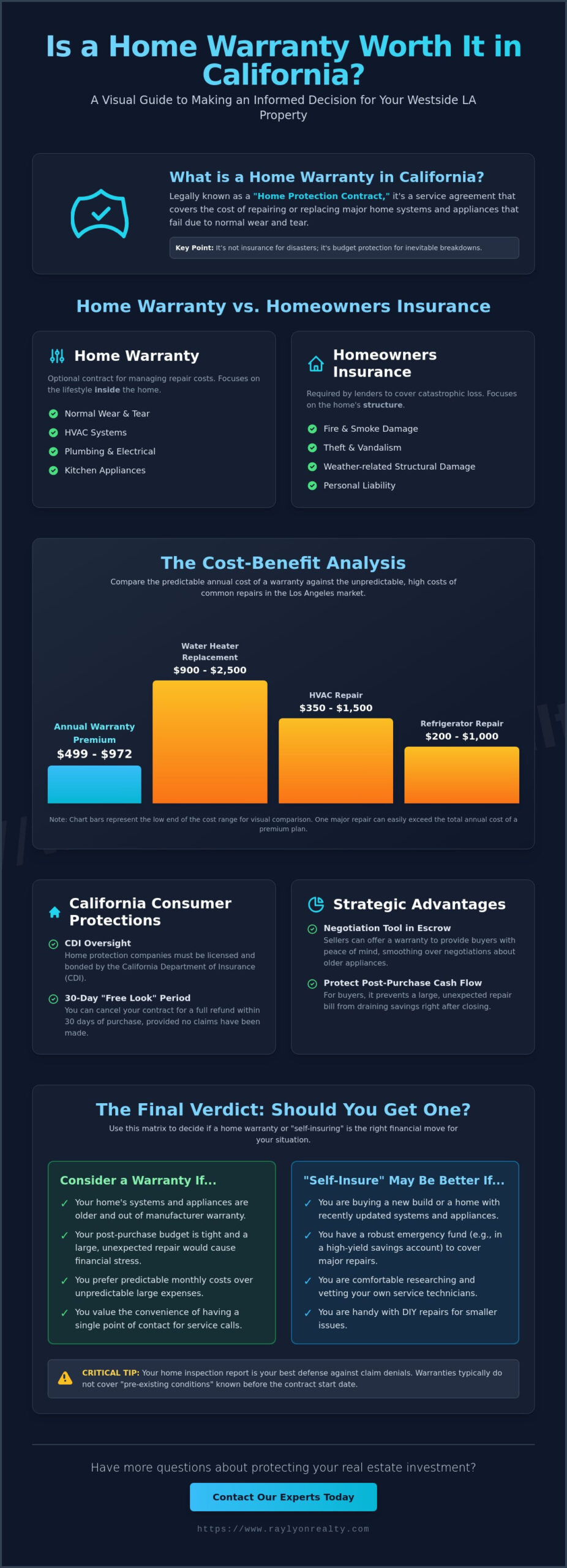

The Cost-Benefit Analysis: California Repair Prices vs. Premiums

Deciding is a home warranty worth it in california requires a hard look at local math. In the high-demand neighborhoods of Westside LA, you aren’t just paying for parts; you’re paying for some of the most expensive specialized labor in the country. A single visit from a licensed plumber in Santa Monica or a certified HVAC tech in Venice can easily exceed $300 before they even open their toolbox. When you compare the average California annual premium of $499 to $972 against the cost of a major system failure, the value proposition shifts quickly.

For example, replacing a tank-style water heater in 2026 typically ranges from $900 to $2,500. If that unit fails six months after you move in, a warranty that costs $70 a month suddenly looks like a brilliant investment. This protection of “post-purchase liquidity” is vital. After stretching your budget for a down payment on a California home, the last thing you need is a $5,000 surprise. Understanding the California regulations for home protection contracts can help you verify that your provider is licensed to operate in this high-stakes market.

Typical Repair Costs in the Los Angeles Market

The Westside is home to a unique mix of architectural eras. In neighborhoods like Mar Vista, many charming homes still feature aging galvanized pipes or original electrical panels that are nearing the end of their functional life. While a home warranty won’t pay to upgrade your entire house, it can bridge the gap when a specific component fails. Consider these 2026 Los Angeles averages:

- HVAC Repair: Mid-level fixes range from $200 to $1,200.

- Appliance Repair: Most visits cost between $150 and $400.

- Service Call Fee: You pay a “deductible” of $65 to $125 per visit.

If you’re evaluating a property with older systems, having an experienced real estate professional by your side can help you spot these potential “money pits” before you sign the contract.

Calculating Your Personal “Break-Even” Point

The “10-Year Rule” is a great starting point for your analysis. If your furnace, water heater, or refrigerator is more than a decade old, the statistical likelihood of a mechanical failure increases sharply. Generally, if you anticipate needing two or more service calls in a twelve-month period, the warranty pays for itself. For first-time buyers, the ROI isn’t just about the dollars saved; it’s about the peace of mind that comes from knowing a single broken dishwasher won’t derail your monthly budget.

Strategic Advantages for California Buyers and Sellers

In the high-stakes environment of Westside LA real estate, a home protection plan often serves as a strategic olive branch during escrow. When negotiating a deal, the question of is a home warranty worth it in california isn’t just about repair costs. It’s about risk management and ensuring a smooth transition of ownership. By including a warranty in the contract, both parties can move toward closing with a higher degree of confidence. For those navigating the nuances of the local market, our Santa Monica Real Estate Guide provides additional context on how these tools fit into a broader purchase strategy.

Using a warranty strategically can mitigate “post-sale friction.” This refers to the uncomfortable phone calls a seller might receive from a buyer when an appliance fails shortly after move-in. When a policy is in place, the buyer has a clear protocol to follow. They contact the service provider directly rather than seeking recourse from the previous owner. This layer of separation is invaluable for maintaining a professional and clean break after the deal is done.

For Sellers: Reducing Liability and Increasing Appeal

Offering a home warranty as part of your listing package can be a powerful marketing tool. It signals to potential buyers that you’ve maintained the property and are willing to stand behind its condition. This can be especially effective in a neutral or buyer’s market where you need every competitive edge. Many providers offer “Seller’s Coverage,” which protects your systems while the home is actively on the market. This ensures that if the AC fails during an open house, you aren’t hit with a massive repair bill before you’ve even secured a buyer. It also provides a way to sidestep minor repair requests during the inspection contingency period by offering the warranty as a comprehensive solution instead.

For Buyers: Protecting Your Investment in Escrow

As a buyer, you can request that the seller pays for a one-year home warranty as a closing cost credit. This is a common practice, particularly when purchasing older inventory in neighborhoods like Mar Vista. These homes often have a mix of charming original features and aging mechanical systems. Because the California Department of Insurance regulates these contracts, you can verify that your chosen plan meets state standards for consumer protection. When selecting your plan, ensure you include add-ons for California-specific needs, such as pool and spa equipment or secondary refrigerator units. This tailored approach ensures your post-closing liquidity remains intact while you settle into your new Westside lifestyle.

Navigating Exclusions: The “Fine Print” and Claim Denials

“They never cover what actually breaks.” It’s the most common complaint I hear from clients when discussing whether is a home warranty worth it in california. This skepticism is often rooted in the frustration of a denied claim during a stressful moment. However, most denials aren’t random; they’re the result of specific contractual exclusions that many homeowners overlook until it’s too late. Understanding these traps before you sign is the difference between a wasted premium and a successful repair.

One of the most significant hurdles in the California market involves code upgrades. Our state has some of the strictest building codes in the country. If your water heater fails and the new installation requires a specific seismic strapping or a different venting system to meet 2026 standards, a basic warranty plan might only cover the cost of the unit itself. You could be left footing the bill for the mandatory upgrades. Always look for “Code Upgrade” coverage in your plan to avoid this specific California surprise.

Common Reasons for Denial in California Homes

Claim denials often boil down to three main categories. First is the “Lack of Maintenance” clause. If you haven’t changed your HVAC filters or flushed your water heater annually, the company may claim the failure was preventable. Second, “Incorrect Installation” is a major issue in Westside LA, where DIY projects and quick property flips are common. If a previous owner installed a dishwasher improperly, the warranty company might refuse to fix it. Finally, there’s “Secondary Damage.” While the warranty might pay to fix a burst pipe, it almost never pays to replace the hardwood floors or drywall ruined by the resulting leak.

How to Ensure Your Claims Get Approved

Your best defense against a denial is a paper trail. Keep every service record and receipt for maintenance performed on your systems. When you’re in the process of buying, your real estate agents in Los Angeles will help you coordinate a professional home inspection. This report is gold; it serves as documented proof that a system was in good working order at the time of purchase, effectively neutralizing the “pre-existing condition” argument. Always read the “Coverage Limits” section of your contract before you call for service so you know exactly what to expect.

If you’re currently navigating a complex escrow and need a strategic partner to review your inspection findings, reach out to our team today for expert guidance on protecting your investment.

The Final Verdict: Is it Worth it for Your California Home?

After weighing the high labor costs of the Westside against the regulatory protections of the Golden State, the question remains: is a home warranty worth it in california? The answer isn’t a simple yes or no. It’s a strategic decision that depends on your specific property, your financial liquidity, and your tolerance for risk. For many, a warranty is a bridge that covers the gap between moving in and building up a healthy home maintenance fund. For others, it’s an unnecessary layer of bureaucracy that gets in the way of using their preferred local contractors.

If you aren’t comfortable with the idea of a third-party company choosing your technician, consider “self-insuring.” This involves taking the $500 to $900 you would have spent on an annual premium and placing it into a dedicated high-yield savings account. This fund stays under your control. If nothing breaks, you keep the interest. If a repair is needed, you have the cash ready to hire the specialist of your choice. However, this requires the discipline to let that fund grow before a major system failure occurs.

When a Home Warranty is Definitely Worth It

There are three specific scenarios where these contracts provide undeniable value in the Los Angeles market:

- First-Time Buyers: If you’ve just exhausted your savings on a down payment and closing costs, you have low cash reserves. A warranty prevents a broken furnace from becoming a financial crisis in your first month of ownership.

- Aging Systems: When a home’s HVAC, water heater, or major appliances are between 8 and 12 years old, they’re entering the statistical “failure zone.” In this case, is a home warranty worth it in california? Almost certainly, as the cost of one repair often exceeds the annual premium.

- Strategic Sellers: Offering a warranty as a “clean transfer” tool can reduce your liability and prevent buyers from nitpicking minor items during the inspection period.

When You Should Probably Skip It

You can likely save your money if your situation matches these criteria:

- New Construction: Most new homes come with a builder’s warranty that covers major systems and structural issues for the first few years.

- Recently Renovated Homes: If you have verified permits showing all major systems were replaced in the last 24 months, the likelihood of a “wear and tear” failure is minimal.

- High Liquidity: If you maintain a robust emergency fund and already have a “short list” of trusted plumbers and electricians, you’ll likely find the warranty process more frustrating than helpful.

Expert Advice from Ray Lyon Realty

Our team understands that every Westside property has its own personality and set of risks. We don’t just help you find a house; we help you protect your investment. During the escrow process, we’ll review your inspection report together to determine if a warranty is a smart negotiation point or a waste of your capital. We’ve seen which local providers honor their contracts and which ones hide behind the fine print. When you’re ready to make a move in Santa Monica or Mar Vista, Contact Ray Lyon Realty to discuss a strategy tailored to your specific financial goals.

Secure Your Westside Property Investment

Deciding is a home warranty worth it in california is a vital step in your homeownership journey. We’ve explored how these contracts serve as a strategic safety net against high Westside labor rates and how they can smooth over the escrow process. Whether you choose a comprehensive plan or decide to self-insure, the goal is to protect your liquidity and enjoy your new home without the fear of a sudden mechanical failure.

Success in the Santa Monica and Mar Vista markets requires more than just finding the right house. It requires a strategic approach to every detail, from property renovation history to complex contract negotiations. Our team brings years of personal experience in flipping and development to ensure you have a competitive edge. We’re here to help you navigate the fine print and secure a deal that works for your long-term financial goals.

Consult with Ray Lyon Realty for Expert Local Real Estate Advice to start your next chapter with confidence. We look forward to helping you find and protect your perfect California property.

Frequently Asked Questions

Does a home warranty cover pre-existing conditions in California?

No, standard home protection contracts do not cover pre-existing conditions that were known or should have been detected during a visual inspection. However, many companies will cover “unknown” pre-existing conditions if the system was in good working order at the time of the home inspection. This is why keeping a copy of your professional 2026 home inspection report is the best way to prove a failure wasn’t a pre-existing issue.

Who typically pays for the home warranty in a California real estate transaction?

Sellers typically pay for the first year of a home warranty as a gesture of good faith during the escrow process. While it’s a common seller-paid closing cost in the Westside market, everything is negotiable. In a highly competitive buyer’s market, a seller might offer a premium plan to stand out; in a seller’s market, a buyer might choose to pay for their own policy to make their offer more attractive.

Can I choose my own contractor with a California home warranty?

Most home warranty companies require you to use a technician from their pre-approved network to ensure they control the repair costs. If you have a preferred local specialist, you must get explicit “out-of-network” authorization from the warranty company before any work begins. Under 2026 California transparency laws, contractors must disclose their subcontractor details, which helps ensure you’re getting qualified labor even when the company chooses the pro.

What is the average cost of a home warranty in Los Angeles?

The average cost for a home warranty in California currently ranges from $42 to $83 per month, or roughly $499 to $972 per year. When asking is a home warranty worth it in california, you must also factor in the service call fee, which typically runs between $65 and $125 per visit. In high-cost areas like Santa Monica, these premiums often lean toward the higher end of the scale to account for local labor rates.

How do I file a complaint against a home warranty company in California?

You should file a formal complaint with the California Department of Insurance (CDI) if a company unfairly denies a claim or fails to provide service. Because home protection contracts are legally regulated as insurance-like products in our state, the CDI has the authority to investigate licensed providers. Always keep a detailed log of your service requests and communication with the company to support your case if a dispute arises.

Does a home warranty cover roof leaks in CA?

Roof leak coverage is rarely included in a base plan and usually requires a specific optional add-on. Even with the add-on, coverage is typically limited to patching leaks over the living area of the home rather than full roof replacement. It’s important to distinguish this from homeowners insurance, which might cover major roof damage caused by a fallen tree or a significant storm event.

Are home warranties required by law in California?

No, home warranties are not required by law, though many real estate professionals consider them a best practice for risk management. While your mortgage lender will mandate homeowners insurance to protect the structure, deciding is a home warranty worth it in california remains an optional choice for the buyer or seller. It’s a private service contract designed to manage the financial impact of mechanical wear and tear.

Is a home warranty the same as a structural warranty for new builds?

No, these are two different types of protection. A home warranty covers appliances and mechanical systems like your HVAC or water heater for a one-year renewable term. A structural warranty is usually provided by the builder of a new construction home and covers the integrity of the foundation, framing, and roof for up to 10 years. If you’re buying a brand-new home, you likely don’t need a separate home warranty for the first few years.