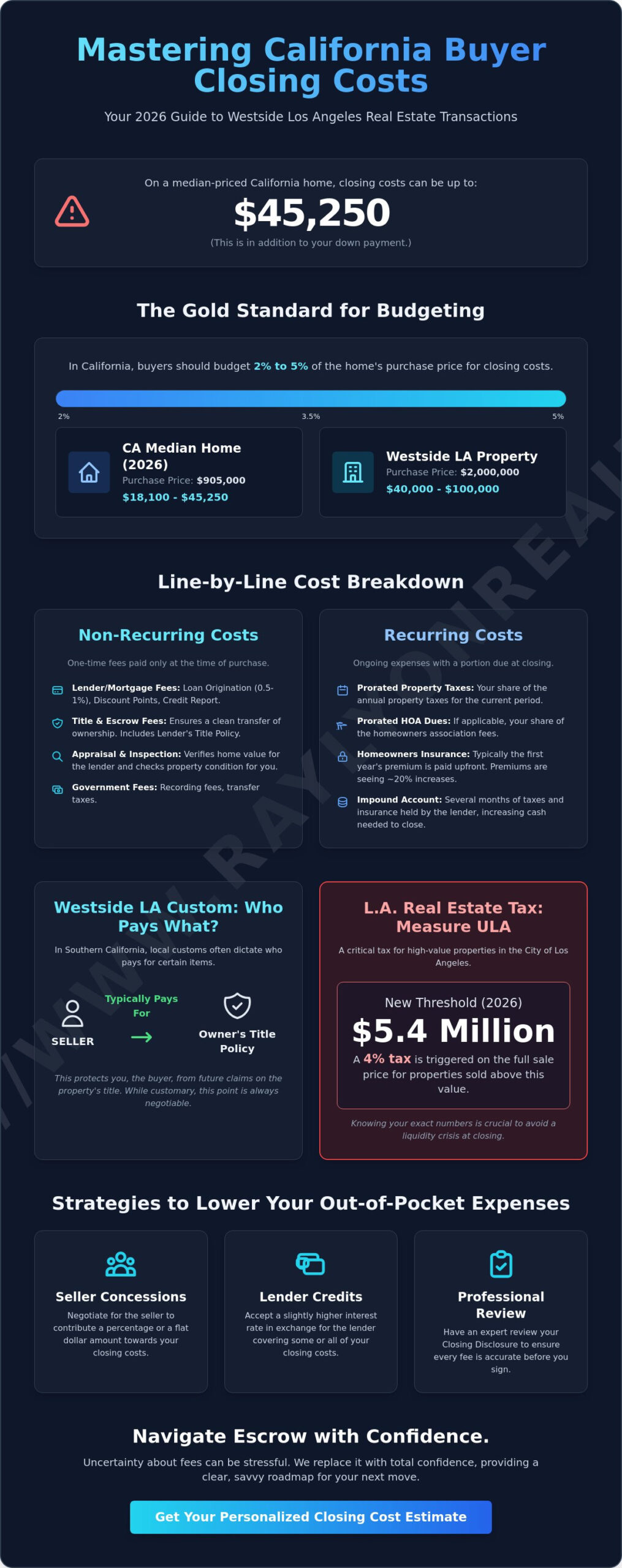

On a median-priced home in California, you might need to bring up to $45,250 to the closing table just to cover fees. It’s a figure that often catches people off guard, especially when you’re already focused on the down payment. Understanding the closing costs for buyer in california is essential to avoiding last-minute stress during escrow.

I know how it feels to see those numbers and wonder if there’s a mistake. It’s completely normal to feel some anxiety about hidden fees or confusion over whether you or the seller should be picking up the tab for title insurance. My goal is to replace that uncertainty with total confidence. I’ll show you exactly how to master these complexities so you can budget with precision.

In this 2026 guide, we’ll break down local Westside LA customs and the newest tax thresholds for Measure ULA. We’ll also look at assistance programs like CalHFA’s Dream For All and share strategic tips to minimize your out-of-pocket expenses. By the time you’re done reading, you’ll have a clear, savvy roadmap for your next move.

Key Takeaways

- Learn why the 2% to 5% rule is the gold standard for budgeting and how to accurately project your closing costs for buyer in california based on your specific purchase price.

- Identify the specific lender and property fees, including Westside-specific inspections, that make up your final line-by-line bill.

- Navigate Southern California customs with ease by understanding why Westside LA sellers typically cover the owner’s title insurance policy.

- Discover proven strategies to lower your out-of-pocket expenses through strategic seller concessions and lender credits.

- Gain a competitive edge with a professional review of your Closing Disclosure to ensure every fee is accurate before you sign.

Understanding Closing Costs in the California Real Estate Market

Closing costs are the bundle of fees, taxes, and insurance you pay at the end of your home purchase. While some national websites might give you a flat dollar amount, Understanding Closing Costs through the lens of a percentage is much more accurate for our local market. In California, buyers should budget between 2% and 5% of the total purchase price. This range accounts for everything from lender fees to government transfer taxes. Getting a handle on the closing costs for buyer in california is the first step toward a stress-free escrow.

Accuracy is vital right now. With the projected median home price in California hitting $905,000 in 2026, even a small percentage fee adds up quickly. In Los Angeles, where Measure ULA thresholds have recently shifted to $5.4 million for the 4% tax, knowing your exact numbers helps you avoid a liquidity crisis at the finish line. You don’t want to find out you’re short on cash three days before you’re supposed to get the keys.

To better understand this concept, watch this helpful video:

The Impact of High Property Values in Westside LA

If you’re looking in Santa Monica or Mar Vista, the 2% to 5% rule feels different. On a $2 million property, you’re looking at $40,000 to $100,000 in closing costs for buyer in california. That is a massive difference compared to state averages. This scale often causes sticker shock for those moving from less expensive regions. Successful buyers here plan their liquidity months in advance. You need to ensure your funds are accessible and not locked in long-term investments that might be difficult to liquidate during a 30-day escrow.

Non-Recurring vs. Recurring Costs

We categorize these expenses into two groups. Non-recurring costs are one-time fees paid only at the time of purchase. These include your home inspection, appraisal, and title insurance. Recurring costs are ongoing expenses that you’ll pay for as long as you own the home, but a portion is due at closing. Think of prorated property taxes, HOA dues, and homeowners insurance. In 2026, insurance premiums are a major factor. Some buyers see 20% increases in their quotes. Many lenders also require an impound account. This is an escrow account where they hold several months of taxes and insurance upfront. It acts as a safety net for the lender, but it increases the amount of cash you need on closing day.

A Line-by-Line Breakdown: What California Buyers Actually Pay

Once you move past the broad estimates, it’s time to look at the specific line items that appear on your Closing Disclosure. Seeing a long list of fees can feel overwhelming, but most fall into a few predictable categories. Understanding the closing costs for buyer in california requires a look at lender requirements, property specifics, and the government’s share of the transaction. Each of these components plays a role in your final “cash to close” figure.

Lender and Mortgage-Related Charges

Your mortgage is often the largest source of closing fees. Most lenders charge a loan origination fee to process your application, which typically ranges from 0.5% to 1% of the loan amount. In 2026, many of my clients are also choosing to pay “discount points.” These are upfront fees paid to lower your long-term interest rate, which can be a savvy move if you plan to stay in your Westside home for several years. You’ll also see smaller charges for your credit report and tax service fees. Be aware that luxury properties in areas like Pacific Palisades often require specialized appraisals. These can cost significantly more than a standard appraisal because the homes are unique and harder to value.

Title Insurance and Escrow Services

Ensuring a clean transfer of ownership is the job of title and escrow companies. There are two types of title insurance: the Lender’s Policy, which you pay for to protect the bank, and the Owner’s Policy, which protects you. In Southern California, it’s customary for the seller to pay for the Owner’s Policy, but this is always negotiable. Escrow fees in Los Angeles usually consist of a base fee plus a rate based on every $1,000 of the purchase price. Don’t forget the “nuisance” costs; notary fees, wire transfer charges, and courier fees might only be a few hundred dollars each, but they add up quickly during the California home closing process.

Government Recording and Transfer Taxes

The government also takes a slice of the transaction. The standard documentary transfer tax in Los Angeles County is $1.10 per $1,000 of the property’s value. However, city-specific taxes can change the math. If you’re buying in Santa Monica, the transfer tax structure differs from Los Angeles proper, and you’ll need to account for those local variations. Finally, the County Recorder charges recording fees to officially document your deed and trust deed. While these are usually the smallest items on the list, they are non-negotiable requirements for legal ownership.

Getting these details right is about more than just numbers; it’s about making sure your investment is protected from day one. If you want a partner who can help you spot errors and negotiate these fees effectively, you can reach out to my team for a personalized consultation.

Southern California vs. Northern California: Who Pays What?

In California, the question of who pays for what isn’t just a matter of law; it’s a matter of tradition. These traditions, often called “customary” splits, change depending on which side of the Tehachapi Mountains you’re on. Understanding these regional quirks is vital when calculating California buyer closing costs. While Northern California buyers often shoulder a heavier burden, Southern California has a long-standing history of splitting the bill more evenly between the buyer and the seller.

The Los Angeles County Standard

In Los Angeles County, the seller traditionally covers the cost of the owner’s title insurance policy and the documentary transfer tax. They also usually pay for the Natural Hazard Disclosure (NHD) report. As a buyer, your primary responsibilities include your loan-related fees, home inspections, and your half of the escrow fee. This 50/50 split of escrow services is a hallmark of the Southern California market. It’s quite different from San Francisco or Riverside County, where it’s common for buyers to pay for the title insurance and the entire escrow fee themselves. If you’re moving from the Bay Area to the Westside, this shift in local custom might actually save you a significant amount of cash.

Pragmatic Shifts in a Competitive 2026 Market

Customs provide a helpful baseline, but they aren’t set in stone. In the high-stakes 2026 market, especially in neighborhoods like Mar Vista or Venice, we often see these traditions fly out the window. If you’re in a multiple-offer situation on a prime property, offering to pick up the seller’s traditional costs can make your bid much more attractive. This is where a strategic Santa Monica real estate agent becomes an invaluable asset. We help you weigh the cost of these concessions against the value of winning the home. It’s about being nimble and knowing when to follow tradition and when to break it to secure the deal.

When you’re calculating the closing costs for buyer in california, don’t assume the seller will automatically follow the local script. If a property has been sitting on the market for a few weeks, we might flip the script and ask the seller to cover your half of the escrow fee or provide a credit for your non-recurring costs. Conversely, in a hot market, you might pay the seller’s transfer taxes just to get your foot in the door. These strategic maneuvers require a deep understanding of current inventory levels and seller motivation on the Westside. My team constantly monitors these micro-market shifts to ensure you aren’t overpaying or missing out on a competitive edge.

Strategies for Reducing Your Out-of-Pocket Expenses at Closing

While the numbers we’ve discussed so far might seem set in stone, you actually have several levers to pull. Reducing your closing costs for buyer in california is a strategic exercise that begins the moment we draft your initial offer. On the Westside, where purchase prices are high, even small adjustments in how fees are allocated can save you tens of thousands of dollars in upfront cash. It’s about being resourceful and knowing which costs are flexible.

The Art of the Seller Concession

A seller concession is a credit the seller provides to cover a portion of your closing expenses. To make this work in a competitive market, we sometimes structure “over-asking” offers. For example, if a home is listed at $1.5 million, you might offer $1.52 million but ask for a $20,000 credit back at closing. This effectively rolls your closing costs into your mortgage. Keep in mind that loan types have strict limits on these concessions. FHA loans often allow up to 6% of the purchase price, while conventional loans usually cap concessions at 3% if your down payment is less than 10%. We’ll need to coordinate closely with your lender to ensure your strategy fits within these regulatory guardrails.

Lender Credits and Interest Rate Arbitrage

If your primary goal is to keep your cash in the bank, lender credits are a powerful tool. In this scenario, you agree to a slightly higher interest rate, perhaps just 0.125% or 0.25% higher, and in exchange, the lender pays a significant portion of your fees. This is a favorite tactic for Mar Vista real estate investors who prefer to keep their capital liquid for renovations or other investments. The key is calculating the “break-even” point. If the higher rate costs you $100 more per month but saves you $10,000 at closing, it takes over eight years for the higher rate to become more expensive. If you plan to sell or refinance before then, the credit is a clear win.

Beyond these big moves, you can also save by shopping for third-party services. You aren’t required to use the first pest inspector or home warranty company suggested. In the 2026 insurance market, shopping for hazard insurance early is particularly critical. Premiums are rising, and finding a competitive quote can significantly lower your recurring costs. Some lenders even offer “no-closing-cost” mortgages, but these are essentially just lender credits under a different name. They aren’t a trap, but they do require a careful look at the long-term interest cost. They can be a perfect tool if you anticipate a short hold time for the property.

Ready to see a custom breakdown of how these strategies could apply to your Westside home search? Contact me today to start building your strategic purchase plan.

Navigating the Westside LA Escrow Process with Ray Lyon Realty

The escrow period on the Westside is often a whirlwind of paperwork and deadlines. At Ray Lyon Realty, we don’t just wait for the final numbers to arrive. We take a proactive, “Escrow-Ready” approach by reviewing your Closing Disclosure (CD) as soon as it’s available. This early review is crucial for managing the closing costs for buyer in california because it allows us to catch errors before they become obstacles. Whether it’s a miscalculated prorated tax or an incorrect lender fee, we find it early so your closing day stays on track. We’ve seen how last-minute surprises can cause unnecessary anxiety, and our goal is to eliminate that stress entirely.

Granular Local Knowledge as a Financial Safeguard

Our team brings a level of precision that only comes from deep local roots. We understand the specific municipal requirements in Santa Monica that might escape a generalist’s notice. When we look at your Preliminary Settlement Statement, we’re scanning for “junk fees” that can quietly inflate your bill. Because I’ve personally invested in and renovated properties across Los Angeles, I look at your closing statement with the same scrutiny I’d use for my own deals. This hands-on experience means we know which fees are standard and which ones are open for a polite but firm challenge. We also leverage our curated network of Westside specialists to ensure your inspections and reports are priced fairly and delivered on time. Having an insider’s perspective ensures you never pay more than necessary to get the deal done.

Next Steps Toward Your Westside Home

As we approach the finish line, we’ll conduct a final walkthrough to ensure the property is in the agreed-upon condition. This is your chance to verify that any requested repairs were completed and the home is ready for move-in. Once that’s settled, you’ll head to the escrow office for the final signing. We stay in constant communication with your lender to manage the delicate “funding and recording” sequence. In California, the deal isn’t officially closed until the deed is recorded at the County Recorder’s office. We monitor this process in real-time so we can call you the moment the keys are officially yours. It’s a complex dance with many moving parts, but our strategic oversight ensures a seamless transition. We’re with you at every step, from the first tour to the final handshake.

Ready to buy on the Westside? Contact Ray Lyon Realty for a strategic buyer consultation.

Your Strategic Path to a Westside Closing

You now have the tools to turn a complex financial hurdle into a managed part of your home purchase. By understanding local customs and the specific math of the Westside, you’re already ahead of most buyers in the 2026 market. Remember that while state averages provide a baseline, your success depends on navigating the unique transfer taxes and escrow splits of Los Angeles. These strategic moves aren’t just theories; they’re the same tactics I use for my own property investments and renovations.

Mastering the closing costs for buyer in california means you can walk into escrow with your eyes open and your budget protected. My boutique team offers deep expertise in the Santa Monica, Mar Vista, and Venice markets. We prioritize transparency so you’re never left wondering about a fee on your statement. Secure your Westside LA dream home with Ray Lyon Realty and let us put our strategic negotiation experience to work for you.

The keys to your new home are within reach. Let’s make sure the journey there is as smooth and predictable as possible. We look forward to helping you navigate this exciting transition with total confidence.

Frequently Asked Questions

What is the average closing cost for a buyer in California?

Buyers in California typically pay between 2% and 5% of the home’s purchase price in total fees. For a median-priced home of $905,000, this equates to a range of $18,100 to $45,250. This percentage covers everything from lender fees to government taxes. It’s a reliable rule of thumb for your initial budgeting and ensures you have enough liquidity before starting your search.

Does the buyer or seller pay for title insurance in Los Angeles County?

In Los Angeles County, it is customary for the seller to pay for the owner’s title insurance policy. However, the buyer is responsible for the lender’s title insurance policy required by the bank. While these are the local traditions, everything in a real estate contract is negotiable. We often review these splits during the offer phase to ensure they align with your financial goals.

Can I include my closing costs in my mortgage?

You cannot technically add closing costs to your total loan amount, but you can use credits to offset the cash needed at closing. You might negotiate a seller credit where the seller pays a portion of your fees in exchange for a higher purchase price. Alternatively, a lender credit allows you to trade a slightly higher interest rate for lower upfront costs. Both methods effectively finance your closing costs for buyer in california over the life of the loan.

What are “prepaid items” in a California real estate closing?

Prepaid items are recurring costs that lenders require you to pay in advance at the time of closing. This usually includes the first full year of homeowners insurance premiums and several months of property taxes held in an impound account. You’ll also pay “per diem” interest to cover the days between your closing date and the end of the month. These are separate from one-time transactional fees.

How much should I budget for home inspections in Santa Monica?

You should budget between $1,500 and $2,500 for a comprehensive suite of inspections on the Westside. While a general home inspection might cost $500 to $700, luxury properties in Santa Monica often require specialized assessments. We recommend adding sewer lateral, fireplace, and mold inspections to your list. Investing in these detailed reports upfront can save you from expensive repairs after you move in.

What is a Closing Disclosure (CD) and when do I receive it?

The Closing Disclosure is a five-page document that outlines the final terms of your loan and all your actual fees. Federal law requires your lender to provide this document to you at least three business days before you sign your final loan documents. This waiting period gives you time to compare the final numbers with the initial Loan Estimate you received when you first applied for your mortgage.

Are closing costs tax-deductible in California?

Most closing costs are not immediately tax-deductible, but mortgage points paid to lower your interest rate are a notable exception. Other costs, like title insurance and recording fees, are typically added to your home’s cost basis. This reduces your taxable capital gains when you eventually sell the property. You should always consult with a tax professional to see how these rules apply to your specific financial situation in 2026.

Can I negotiate the escrow fee in Southern California?

You can negotiate who pays the escrow fee, though a 50/50 split is the standard custom in Southern California. If you are in a strong negotiating position, you can ask the seller to cover your half of the fee. You also have the right to shop around for different escrow companies. However, in many transactions, the choice of escrow is a point of negotiation between the buyer and seller during the offer process.