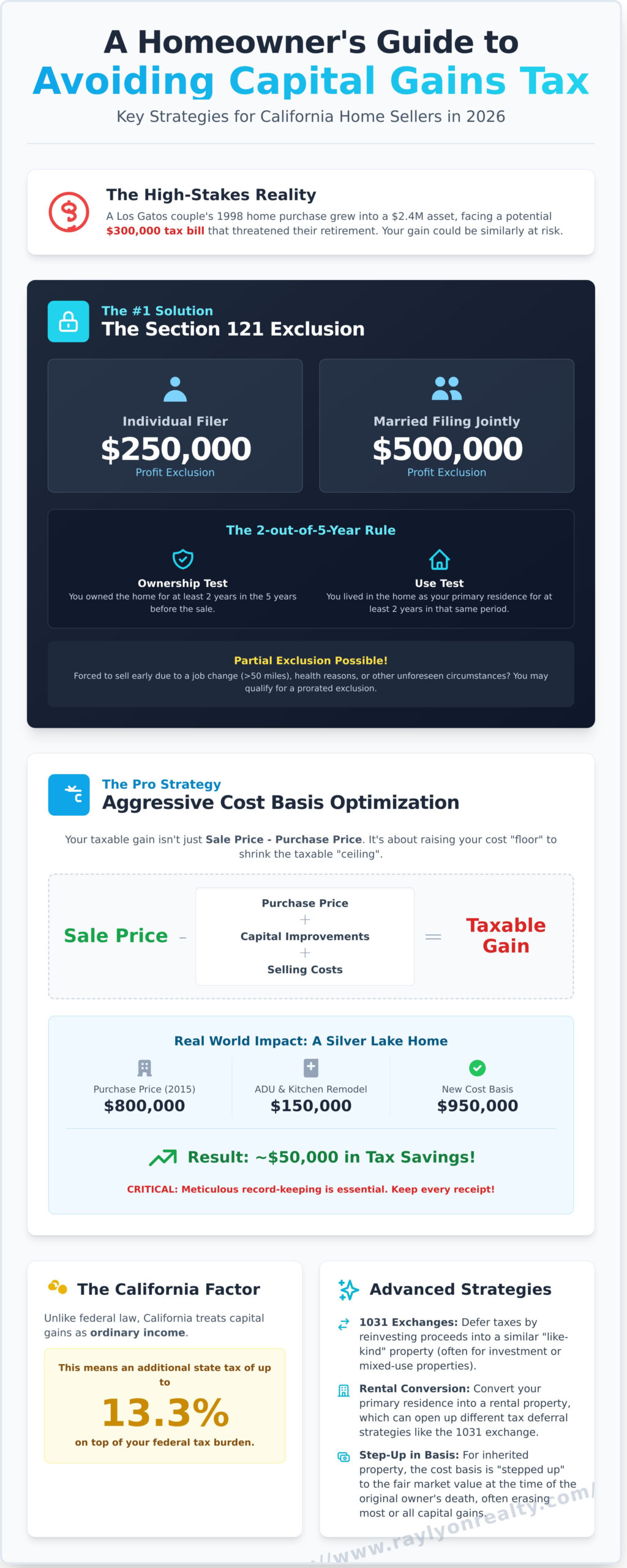

Last Tuesday, a couple in Los Gatos realized their 1998 home purchase had ballooned into a $2.4 million asset, leaving them with a potential tax bill that could wipe out $300,000 of their retirement fund. If your home’s value has climbed past the $500,000 exclusion limit, you’re likely feeling that same mix of excitement and anxiety. You’ve spent years building equity, and it’s frustrating to think a huge chunk of your nest egg might vanish. This 2026 guide reveals the exact legal strategies for avoiding capital gains tax on home sale california so you can keep your hard-earned proceeds.

California treats capital gains as ordinary income, which means the state can take up to 13.3% on top of federal hits. It’s a heavy burden, but you don’t have to settle for a smaller check at closing. We’ll dive into how $50,000 in specific kitchen renovations can lower your tax bill, how the step-up in basis works for inherited property, and how to navigate the messy overlap between federal and state tax codes. Let’s make sure you walk away with every dollar you deserve.

Key Takeaways

- Learn how to maximize the Section 121 exclusion to shield up to $500,000 of your home equity from federal taxes in 2026.

- Master the formula for aggressive cost basis optimization to significantly lower your taxable gain by accounting for improvements and selling costs.

- Navigate the Franchise Tax Board’s unique “ordinary income” rules and discover the most effective legal strategies for avoiding capital gains tax on home sale california.

- Explore advanced wealth-building tactics, such as “Mixed-Use” 1031 exchanges and rental conversions, to protect your profit long-term.

- Discover how “block to block” local expertise and a strategic contractor network can help you maximize your home’s value while minimizing your tax hit.

The Foundation: Understanding the Section 121 Exclusion in 2026

Selling a home in the current California market feels like a high-stakes financial maneuver. For most homeowners on the Westside, your house isn’t just a shelter; it’s your largest investment. The IRS Section 121 exclusion is your primary tool for protecting that investment. This federal rule allows individuals to exclude up to $250,000 of profit from their taxable income. If you’re married and filing jointly, that threshold jumps to $500,000. In a city where a modest bungalow in Mar Vista can appreciate by half a million dollars in less than a decade, these numbers are vital.

The IRS Section 121 exclusion is a cornerstone of the Capital Gains Tax in the United States, specifically designed to protect your primary equity. To qualify, you must pass the 2-out-of-5-year rule. This means you must have owned and lived in the home as your primary residence for at least 24 months out of the five years leading up to the sale date. These 24 months don’t need to be consecutive. You can live there for a year, rent it out for two, and then move back in for another year to meet the requirement. Understanding the Section 121 exclusion is the first step toward avoiding capital gains tax on home sale california.

For homeowners in high-value areas like Pacific Palisades or Santa Monica, this exclusion is powerful but sometimes insufficient. If your gain exceeds the $500,000 limit, you’ll owe taxes on the remaining balance. However, by maximizing this foundation, you ensure that the first half-million of your profit stays in your pocket rather than going to the treasury.

The ‘Ownership and Use’ Test: Avoiding Common Pitfalls

To satisfy the IRS, you must prove both ownership and use. Ownership is simple; your name must be on the title. Use is more nuanced. You must physically occupy the property as your main home for 730 days within the five-year window. I’ve seen clients struggle with this when they try to claim the exclusion on a second property in Malibu. If you only spend weekends there, it’s a vacation home, not a primary residence. The IRS looks at where you’re registered to vote and the address on your driver’s license. There are generous exceptions for service members on qualified official extended duty. They can suspend the five-year period for up to 10 years. Similar leniency exists for individuals with certain disabilities who must move into a care facility.

The Partial Exclusion: What if You Sell Early?

Life doesn’t always wait for a two-year anniversary. If you’re forced to sell before hitting the 730-day mark, you might still qualify for a prorated exclusion. While the rules are strict, avoiding capital gains tax on home sale california remains possible even if you haven’t hit the full two-year mark. The IRS provides ‘Safe Harbor’ rules for specific scenarios. If you move because your new job is at least 50 miles farther from your home than your old job, you can claim a partial exclusion. Health-related moves, such as relocating to care for a sick family member, also qualify. You’ll need solid documentation, like a doctor’s letter or an employment contract, to prove the sale was a necessity rather than a choice. If you lived in the home for 12 months instead of 24, you’d generally be eligible for 50% of the exclusion amount.

Aggressive Cost Basis Optimization: The Secret to Reducing Taxable Gain

Most California homeowners focus solely on the $250,000 or $500,000 exclusion. While those numbers are vital, they’re only half the story. The real strategy for avoiding capital gains tax on home sale california lies in aggressively optimizing your cost basis. Think of your cost basis as the “floor” of your investment. The higher you can legitimately push that floor, the smaller your taxable “ceiling” becomes. The math is simple: Sale Price minus (Original Purchase Price + Improvements + Selling Costs) equals your Taxable Gain.

At Ray Lyon Realty, we often talk about “putting lipstick” on a property to get it ready for market. While fresh paint and modern fixtures attract buyers, these “Strategic Upgrades” also serve a dual purpose. When done correctly, they’re not just marketing expenses; they’re investments that reduce your tax liability. If you bought a home in Silver Lake for $800,000 in 2015 and spent $150,000 on a permitted ADU and kitchen remodel, your basis isn’t $800,000 anymore. It’s $950,000. That $150,000 difference could save you roughly $50,000 in combined state and federal taxes depending on your bracket.

Meticulous record-keeping is your best friend here. Every contractor receipt, permit fee, and material invoice is worth its weight in gold. If you can’t prove the expense, the IRS won’t count it. We recommend keeping a digital folder of every major project invoice from the day you close escrow. You can find the full list of what the government considers a qualifying expense in IRS Publication 523, which serves as the definitive guide for these calculations.

Capital Improvements vs. Maintenance: What Counts?

The IRS makes a sharp distinction between “improvements” and “repairs.” An improvement adds value, prolongs the home’s life, or adapts it to new uses. Fixing a broken window is maintenance; replacing all windows with energy-efficient dual-pane glass is a capital improvement. Deductible upgrades include new roofs, HVAC systems installed after 2020, and complete bathroom overhauls. However, you should be careful with “selling costs.” Professional staging and minor cosmetic touch-ups like filling nail holes don’t increase your basis. Instead, they’re deducted as costs of the sale. Both reduce your tax, but they go in different columns on your tax return.

Selling Expenses: Deducting the Cost of the Transaction

The costs associated with the transaction itself are often overlooked but highly effective for avoiding capital gains tax on home sale california. Broker commissions are a primary example. When you work with us, our fees are essentially “subsidized” by the tax savings they create because they’re deducted directly from your gross sale price. Other deductible expenses include:

- Legal fees and escrow costs.

- Title insurance and survey fees.

- Advertising and marketing expenses.

- Transfer taxes, including the local Los Angeles Measure ULA.

As of April 1, 2023, the Measure ULA “mansion tax” adds a 4% tax on sales over $5.15 million and 5.5% on sales over $10.3 million. These are massive numbers, but they’re also fully deductible selling expenses. If you’re planning a move soon, you can request a custom valuation to see how these local taxes and your current basis will impact your net walk-away number. Understanding these line items before you list ensures you aren’t surprised by a tax bill you didn’t prepare for.

The California Factor: How the Franchise Tax Board Differs

California doesn’t play by the same rules as the federal government. While the IRS gives you a break on long-term assets, the Franchise Tax Board (FTB) treats your home sale profit just like your monthly paycheck. This means your gain is taxed as ordinary income. For many of my clients in high-value neighborhoods, this results in a state tax rate as high as 13.3%. It’s a significant hit that many sellers don’t see coming until the escrow papers are signed.

Does California help you out at all? Yes. The state generally conforms to federal law regarding the primary residence exclusion. You can still exclude up to $250,000 if you’re single or $500,000 if you’re married. You should review the California FTB Guidelines on Home Sales to see how these exclusions apply to your specific filing status. Even with this “free” money, a large profit often spills over into taxable territory. This is why avoiding capital gains tax on home sale california requires a more aggressive strategy than in other states.

If you’re planning on moving to a tax-free state like Nevada or Texas before you close, be careful. California uses a “source income” rule. Since the property is physically located in California, the FTB claims its share regardless of where you live on closing day. You can’t outrun the tax man by simply changing your zip code before the sale. You need a dual-strategy approach. The IRS cares about your holding period; the FTB cares about your total annual income and residency status.

High-Income Earners and the Mental Health Services Act Tax

If your taxable income exceeds $1 million, California adds a 1% surcharge. This is the Mental Health Services Act tax. Imagine selling a legacy home in Santa Monica for $3.5 million that you bought for $600,000 in the 1990s. That $2.9 million gain doesn’t just push you into the 13.3% bracket. It triggers that extra 1% “Millionaire’s Tax” on every dollar over the million-mark. Sellers often try to manage this by timing the sale to a year when their other income is lower or by using installment sale methods to spread the gain over two tax years.

Prop 19 and Property Tax Basis Transfers

Since April 1, 2021, Proposition 19 has changed the landscape for homeowners aged 55 and older. You can now take your low property tax basis from your current home and move it to a new primary residence anywhere in California. While this doesn’t directly eliminate the capital gains tax on the sale, it creates a massive long-term financial advantage. For a Los Angeles downsizer, moving a 1980s-era tax basis to a new $2 million condo can save $18,000 or more in annual property taxes. It’s a strategic move that makes avoiding capital gains tax on home sale california less painful because your ongoing carrying costs drop so significantly.

- Ordinary Income: California lacks a lower “long-term” rate for gains.

- Dual Strategy: You must plan for both IRS and FTB rules simultaneously.

- Surcharge: Watch out for the 1% tax on gains over $1 million.

- Prop 19: Use tax basis portability to offset the cost of selling.

I always tell my clients that the FTB is often more rigorous than the IRS. They track property transfers closely. If you don’t have a plan for that 13.3% top rate, you’re leaving a massive amount of your equity on the table. Don’t let a lack of planning turn your hard-earned equity into a gift for the state.

Advanced Strategies: 1031 Exchanges and Step-Up in Basis

While Section 121 covers your personal space, high-value Westside properties often require more sophisticated maneuvers. If your home’s value has climbed by $2 million since you purchased it in 1998, the standard exclusion won’t cover the entire bill. You need a deeper playbook. One effective method involves converting a primary residence into a rental property. By moving out and leasing the home for a minimum of 24 months, you can qualify for a 1031 Exchange. This allows you to defer 100% of your federal and state taxes by reinvesting the proceeds into a “like-kind” investment property.

Installment sales offer another path for avoiding capital gains tax on home sale california by spreading the tax liability over several years. Instead of taking a lump sum, you act as the lender and receive payments from the buyer over a set period, such as 5 or 10 years. You only pay capital gains tax on the portion of the principal you receive each year. This keeps your annual income lower, potentially preventing you from hitting the top 20% federal capital gains rate or the 13.3% California mental health services tax bracket.

The Mixed-Use Property Strategy

You can combine tax codes if your property serves two purposes. Consider a Santa Monica duplex valued at $4.5 million where you live in one unit and rent the other. You can apply the Section 121 exclusion to your living quarters and use a 1031 Exchange for the rental portion. This strategy also applies to homes with a permitted Accessory Dwelling Unit (ADU). If 30% of your property’s square footage is a dedicated rental, 30% of your gain can be rolled into a new investment tax-free. I’ve helped clients use this specific split to transition from large family estates into smaller homes while building a separate retirement portfolio.

Inherited Homes and Death of a Spouse

The “Step-Up in Basis” is the most powerful tax shield in the California real estate market. When a property owner passes away, the “cost basis” of the home resets to the current fair market value. If a couple bought a Pacific Palisades home for $250,000 in 1985 and it’s worth $5 million today, the basis “steps up” to $5 million upon death. In California, a community property state, surviving spouses often receive a “double step-up,” meaning the entire property’s basis resets when the first spouse passes. This allows the survivor to sell the home immediately with $0 in taxable capital gains.

- The 2-Year Grace Period: A surviving spouse can still claim the full $500,000 joint exclusion if they sell the home within 24 months of their partner’s death.

- The Deed Trap: Many parents mistakenly add their children to the home’s deed while still alive. This is a costly error. Doing so forces the child to inherit the parent’s original low-cost basis, leading to a massive tax bill later. It’s almost always better to pass the property through a living trust to ensure the heirs get the full market value step-up.

- Appraisal Importance: Always get a formal appraisal within 90 days of a death to lock in that new basis for the IRS.

These strategies require precise timing and documentation to satisfy both the IRS and the California Franchise Tax Board. If you’re looking to maximize your net proceeds in the current market, get a custom equity analysis to see which strategy fits your specific property and financial goals.

Preparation and Execution: The Ray Lyon Realty Competitive Advantage

Real estate on the Westside isn’t a monolith. A home on a quiet cul-de-sac in Mar Vista commands a different strategy than a bungalow three blocks away near the commercial hub of Venice Boulevard. This block to block knowledge is the foundation of how we help clients. When you’re avoiding capital gains tax on home sale california, your agent’s familiarity with local comparable sales affects more than just the list price. It dictates how we position your home’s value to appraisers to justify a price point that maximizes your $250,000 or $500,000 federal exclusion. Since 2019, I’ve seen Westside values climb by over 40 percent, making these tax thresholds easier to hit and harder to manage without a precise plan.

I’ve built my own home and flipped over 15 properties personally, so I don’t just look at your house as a listing. I look at it as an investment vehicle. We leverage a vetted network of 12 local contractors to handle everything from minor repairs to major capital improvements before the first open house. This isn’t about just putting “lipstick” on the property to make it look pretty. We focus on documented capital improvements that can be added to your cost basis. If we spend $65,000 on a permitted kitchen remodel or a new roof, that investment potentially reduces your taxable gain dollar-for-dollar. It’s a dual-purpose strategy: we drive up the sale price while simultaneously lowering the amount the IRS can touch.

Timing is the most overlooked variable in the tax equation. The IRS 2-out-of-5-year rule is strict. If you move out of your Santa Monica primary residence to a rental but wait too long to sell, you could lose a massive tax break. We analyze your specific residency dates to ensure you list at the optimal moment. In 2023, we helped a family delay their closing by just 14 days to meet the two-year occupancy requirement, saving them nearly $95,000 in unnecessary taxes. That is the difference between a standard agent and a strategic partner.

Maximizing Net Proceeds, Not Just Sale Price

The highest offer on the table isn’t always the one that puts the most money in your pocket after the state and federal government take their share. We analyze every offer through a tax-efficient lens. Sometimes, negotiating a credit for repairs instead of a price reduction is the smarter move for your specific cost-basis calculations. My personal experience with high-end flips in Mar Vista has taught me that the “walk-away” number is the only metric that matters. We don’t just chase the headline-grabbing price; we protect your bottom line by understanding how credits and prorations impact your final settlement statement.

Your Next Steps in the Westside LA Market

Success in the 2024 market requires looking forward to your next move while closing the current chapter. We provide an “insider” advantage by sourcing off-market deals for your replacement home or 1031 exchange through our private network of Westside owners. This prevents you from being squeezed in a high-pressure public bidding war. Our team provides a comprehensive Home Value report that integrates your potential tax liability into the valuation. We also provide direct introductions to three of the top real estate CPAs in Los Angeles who specialize in California-specific tax mitigations.

Ready to protect your hard-earned equity and plan your next move with confidence? Contact Ray Lyon for a Strategic Equity Analysis to see exactly how much you can save.

Secure Your Financial Future in the 2026 California Market

Navigating the 2026 real estate landscape requires more than just luck; it demands a tactical approach to the IRS Section 121 exclusion. By documenting every dollar spent on capital improvements, you can significantly raise your cost basis and protect your equity from the Franchise Tax Board. Whether you’re utilizing the $500,000 joint filing exclusion or exploring 1031 exchange strategies for your investment portfolio, the right preparation ensures you keep more of your wealth. Avoiding capital gains tax on home sale california is entirely possible when you combine strategic tax planning with a deep understanding of local market dynamics.

Ray Lyon brings 15 years of personal experience flipping properties and building homes from the ground up to every client interaction. This block-to-block knowledge of Santa Monica and Mar Vista, combined with expertise in trust sales and 1031 exchanges, provides a distinct competitive advantage. We’ve helped hundreds of local homeowners maximize their net proceeds by focusing on the details that others miss. Ready to sell? Get a professional strategy session with Ray Lyon today. You’ve worked hard for your equity, and it’s time to ensure you keep it where it belongs.

Frequently Asked Questions

Is the $500,000 capital gains exclusion still available in 2026?

Yes, the Section 121 exclusion remains part of the federal tax code for 2026. Single filers can exclude $250,000 of profit, while married couples filing jointly can exclude up to $500,000. Since the Tax Cuts and Jobs Act of 2017 didn’t set an expiration date for this specific provision, it’s a reliable tool for your future financial planning.

Does California tax capital gains differently than the Federal government?

California is one of the few states that treats capital gains as ordinary income, meaning you’ll pay your top marginal tax rate on the profit. While the IRS uses specific long-term rates of 0%, 15%, or 20%, the California Franchise Tax Board taxes these gains at rates reaching 13.3% for high earners. This makes avoiding capital gains tax on home sale california a top priority for protecting your hard-earned equity.

Can I avoid capital gains tax if I use the proceeds to buy another home?

No, the old “rollover” rule that allowed homeowners to defer taxes by purchasing a more expensive home was repealed in 1997. Today, you must qualify for the Section 121 exclusion to keep your profits tax-free. If your gain exceeds the $250,000 or $500,000 limit, you’ll owe taxes on the remainder even if you reinvest every dollar into a new Santa Monica property.

What home improvements are tax-deductible when I sell my California house?

You can’t deduct “lipstick” repairs like interior painting or carpet cleaning, but capital improvements that add value are added to your cost basis. Adding a $45,000 ADU, replacing a 20-year-old roof for $18,000, or installing a $12,000 HVAC system all qualify. These expenses lower your taxable gain, so keep every receipt from your contractors to prove these costs to the IRS.

How does Proposition 19 affect my capital gains tax in California?

Proposition 19, which took effect in April 2021, primarily changes property tax basis transfers rather than capital gains tax. It allows homeowners over 55, or those with severe disabilities, to move their lower property tax base to a new home anywhere in the state. While it won’t eliminate the tax on your sale profit, it significantly reduces your annual carrying costs in your next home.

What happens if I sell my home before living in it for two years?

Selling before the 24-month mark usually means you’ll lose the full $250,000 or $500,000 exclusion. However, you might qualify for a partial, pro-rated exclusion if you’re moving for a job change located 50 miles further away, specific health reasons, or “unforeseen circumstances” like a divorce. If you lived in the home for 12 months, you’d typically be eligible for 50% of the exclusion amount.

How do I calculate the cost basis for my Santa Monica home?

Start with your original 2015 purchase price of $1,250,000 and add your initial closing costs like title insurance and escrow fees. Then, add the $90,000 you spent on that kitchen remodel and the $25,000 for the new hardscaping. This total “adjusted basis” is what you subtract from your final sale price, which is the most effective way of avoiding capital gains tax on home sale california.

Can I use a 1031 exchange on my primary residence in Los Angeles?

No, Section 1031 of the Internal Revenue Code is strictly reserved for investment or business properties. You can’t use it for a home you live in as your main residence. If you’ve converted your Los Angeles home into a rental property for at least 12 to 24 months, you might then qualify to swap it for another investment property while deferring the taxes.